The selection of Mojtaba Khamenei as Supreme Leader after his father’s death in the February 2026 U.S.-Israeli airstrikes on Tehran did not resolve Iran’s legitimacy crisis. It clarified and hardened it. His appointment took place in wartime chaos, with little procedural transparency, which immediately raised questions about how the Assembly of Experts reached its decision, whether in person, through remote voting, or through some form of emergency consultation behind closed doors. The result of that process is not a leader with grounded clerical legitimacy. What emerged is a figure whose authority rests on IRGC sponsorship. That dependency sits at the center of this scenario. The real issue is not simply whether Mojtaba is weak. The real issue is what follows when the generals who elevated a lightweight in clerical robes decide they no longer need the robes at all.

This is not some detached hypothetical. It sits squarely inside the range of plausible outcomes already visible in Iran’s current trajectory. The path toward a hard-right shift into direct military rule has been discussed for some time, with Egypt and Pakistan standing out as the most useful comparative models. Those are not perfect analogies, but they are directionally instructive. Both represent highly repressive systems with deep social inequality, weak public legitimacy, entrenched military institutions, and a governing structure that relies more on force and patronage than on ideological conviction. The scenario here follows that same logic. The IRGC first uses Mojtaba as a transitional cover. Then, once the utility of clerical theater fades, it either sidelines him, strips him of relevance, or removes him entirely, moving into direct bargaining with Washington on military terms.

The Fracture Lines Inside the Islamic Republic

Mojtaba’s Structural Weakness

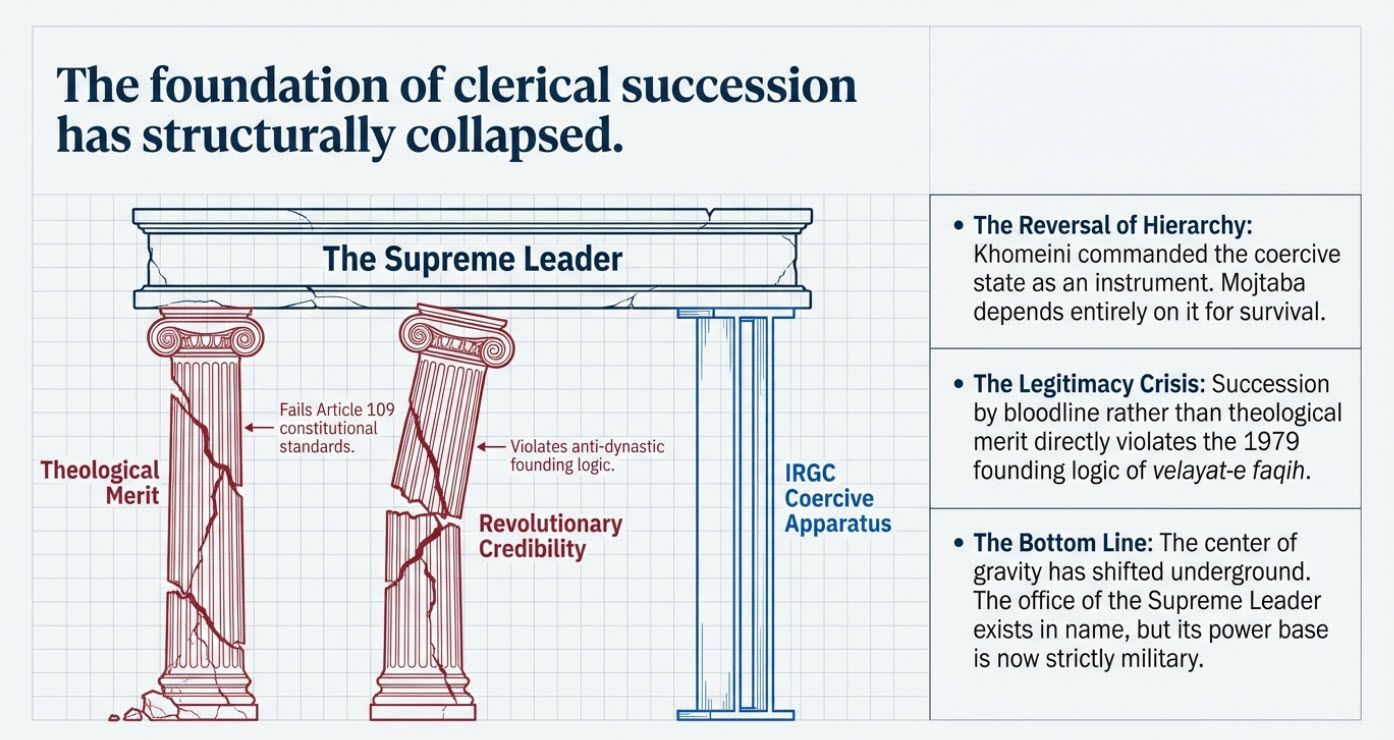

Mojtaba Khamenei’s problem is not simply public perception. His weakness is structural, and it sits at both the theological and political levels. Under Article 109 of the Iranian Constitution, the Supreme Leader is supposed to possess justice, political insight, and administrative capability. The original constitutional structure also required recognition as a grand ayatollah, though that standard was weakened in 1989 to accommodate Ali Khamenei’s own thin clerical credentials. Mojtaba does not meet even that lowered threshold convincingly. He spent more than a decade teaching advanced jurisprudence seminars beginning in 2009, but those efforts were widely viewed as an engineered attempt to manufacture clerical standing rather than the product of genuine scholarly elevation. Senior figures in Qom reportedly objected, and he abandoned those classes in September 2024 amid intensifying succession speculation.

His power base, then, is not religious scholarship. It is not broad political legitimacy. It is not organic revolutionary credibility. His power base is the security apparatus that enabled his succession in the first place. That fact matters because it reverses the Islamic Republic's intended hierarchy. Khomeini used the IRGC as an instrument. Mojtaba depends on the IRGC for survival. Khomeini commanded the coercive state. Mojtaba is a product of it. That is a different kind of Supreme Leader entirely. It means the office still exists in name, but the center of gravity has shifted underneath it.

This is not simply a weak succession. It is a structural inversion of the system’s original design.

The Revolutionary Betrayal Problem

The 1979 Islamic Revolution overthrew the Pahlavi monarchy in part because hereditary succession was framed as illegitimate within an Islamic political order. The system justified itself through velayat-e faqih, the doctrine that governance should rest with qualified jurists acting on behalf of the Hidden Imam. Mojtaba’s rise through bloodline rather than theological merit strikes directly at that founding logic. This is not a minor contradiction. It is an ideological rupture.

That rupture is intensified by the divide between Najaf and Qom. Najaf’s quietist clerical tradition has long stood in tension with Iran’s revolutionary and state-aligned model of clerical rule. As the Iranian system has become more securitized and less theological, that divide has widened. The succession to Mojtaba accelerates that trend. It further exposes the reality that loyalty and institutional control now matter more than religious standing. Once a system crosses that threshold, its ideological shell starts to hollow out.

This creates a separate problem inside the IRGC itself. The organization is not monolithic. Some of its older and mid-generation cadres built their careers on a revolutionary narrative rooted in sacrifice, war, anti-monarchical legitimacy, and ideological mission. For them, dynastic succession is not merely awkward. It is degrading. It turns the founding story into a farce. Add to that the resentment younger, more operationally hardened IRGC elements already feel toward older insiders whose careers drifted into graft and patronage, and the result is a constituency inside the Guard that may prefer a direct military order over the decaying pretense of theocracy. A straight military state at least removes the hypocrisy. From their standpoint, that has a kind of brutal coherence.

The IRGC’s Economic Imperative

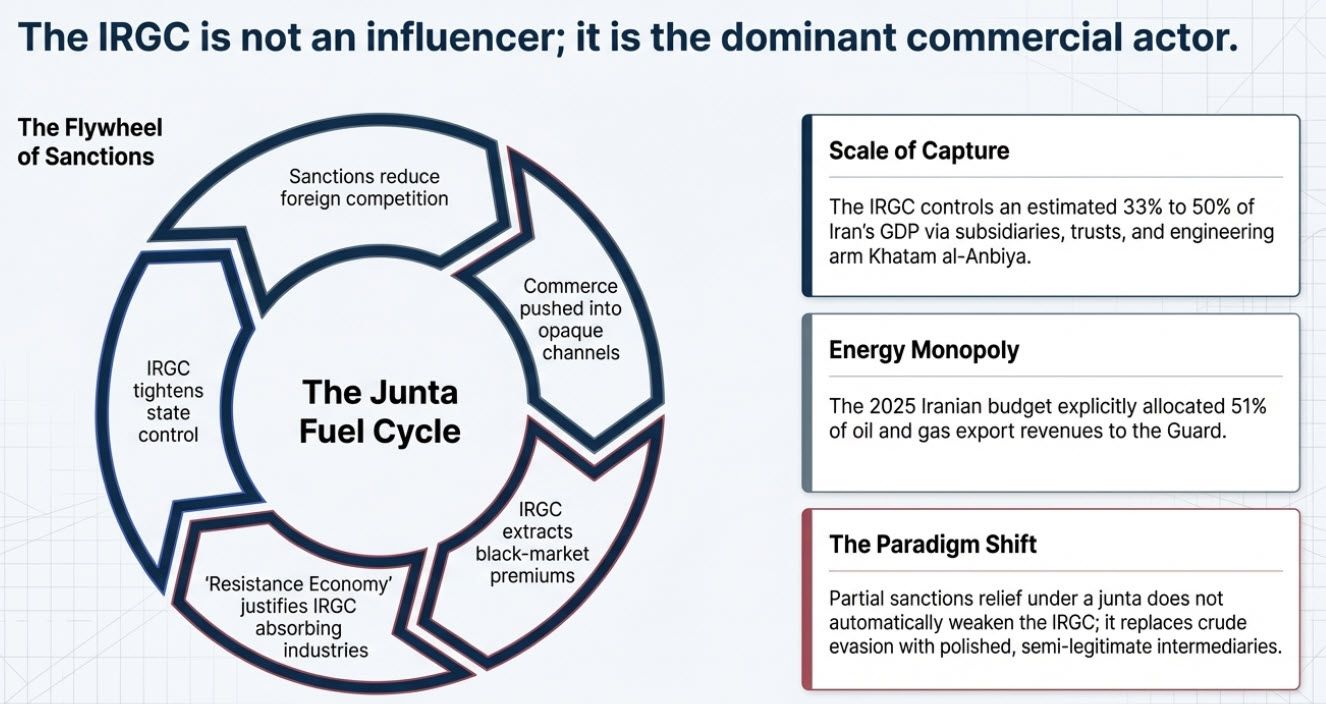

The IRGC’s drive toward full formal control is not only political. It is economic and institutional. This is where many surface-level analyses stop too early. They describe the IRGC as influential. That understates the issue. The IRGC is not simply influential inside Iran’s economy. It is embedded in the core operating systems of the state’s economic life. Estimates have long suggested that the organization controls roughly one-third of Iran’s economy through subsidiaries, trusts, foundations, contracting networks, and opaque commercial structures. Other assessments have suggested that IRGC-linked foundations accounted for more than half of Iran’s GDP as early as 2013. In the 2025 Iranian budget, the IRGC was explicitly allocated 51% of oil and gas export revenues. Up to 50% of Iranian oil exports are estimated to move through IRGC-controlled channels. Its engineering arm, Khatam al-Anbiya, sits across oil, gas, dams, transportation, water distribution, communications, and strategic infrastructure. The Guard also controls borders, ports, and airfields, which gives it command over licit and illicit trade flows alike.

This is not ordinary corruption. It is a parallel political economy. The IRGC does not merely guard the state. It extracts from the state, arbitrages the state, and increasingly functions as the state’s dominant commercial actor. That changes the logic of transition.

Seen clearly, the system is not a state with military contamination. It is a military-commercial structure with a shrinking clerical wrapper.

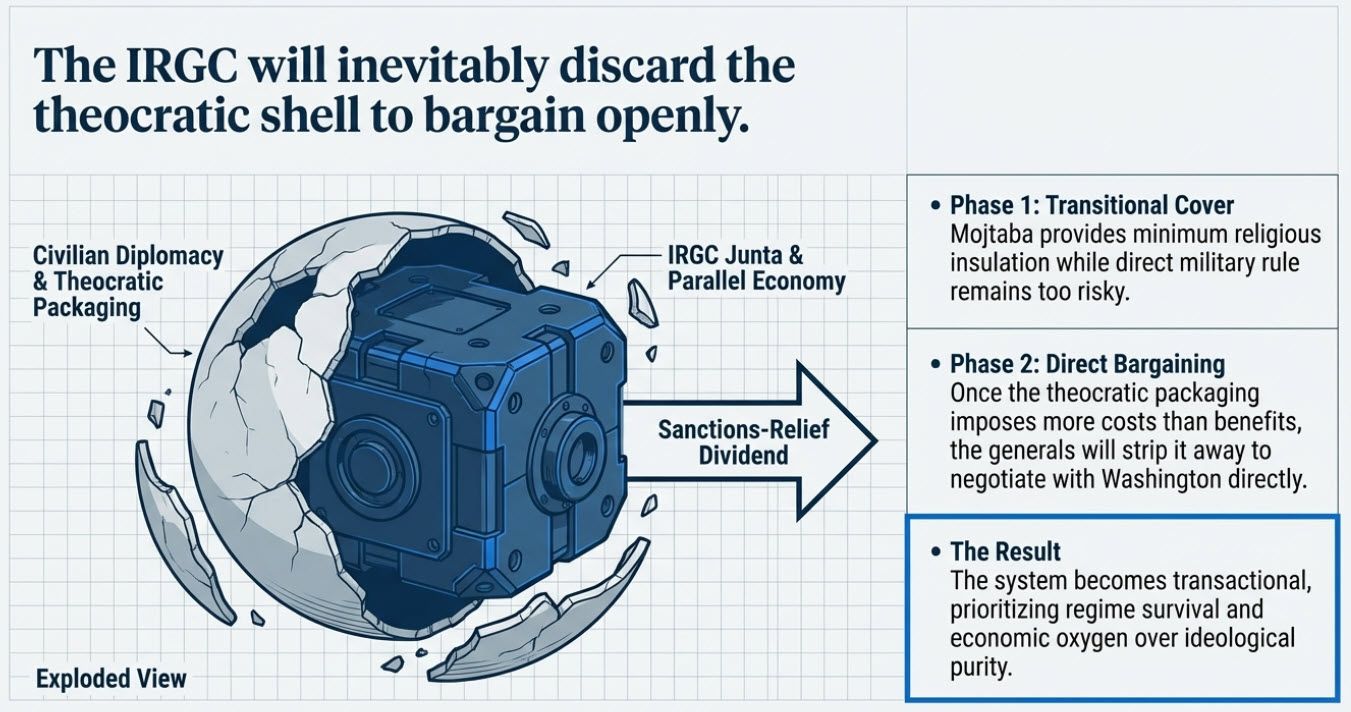

Mojtaba’s value to this system lies in his ability to provide a minimum level of religious cover during a period when open military rule still carries a legitimacy risk. He is useful as a layer of symbolic insulation. But once that insulation becomes less valuable than the costs it imposes, especially if a negotiation track with Washington offers a sanctions-relief dividend, the rational move for the generals is to strip away the theological packaging and bargain openly as the actual holders of power.

The question is no longer whether the Guard sits behind the system. The question is when it decides to stop hiding behind it.

The Environmental Landscape

What the World Looks Like Around This Scenario

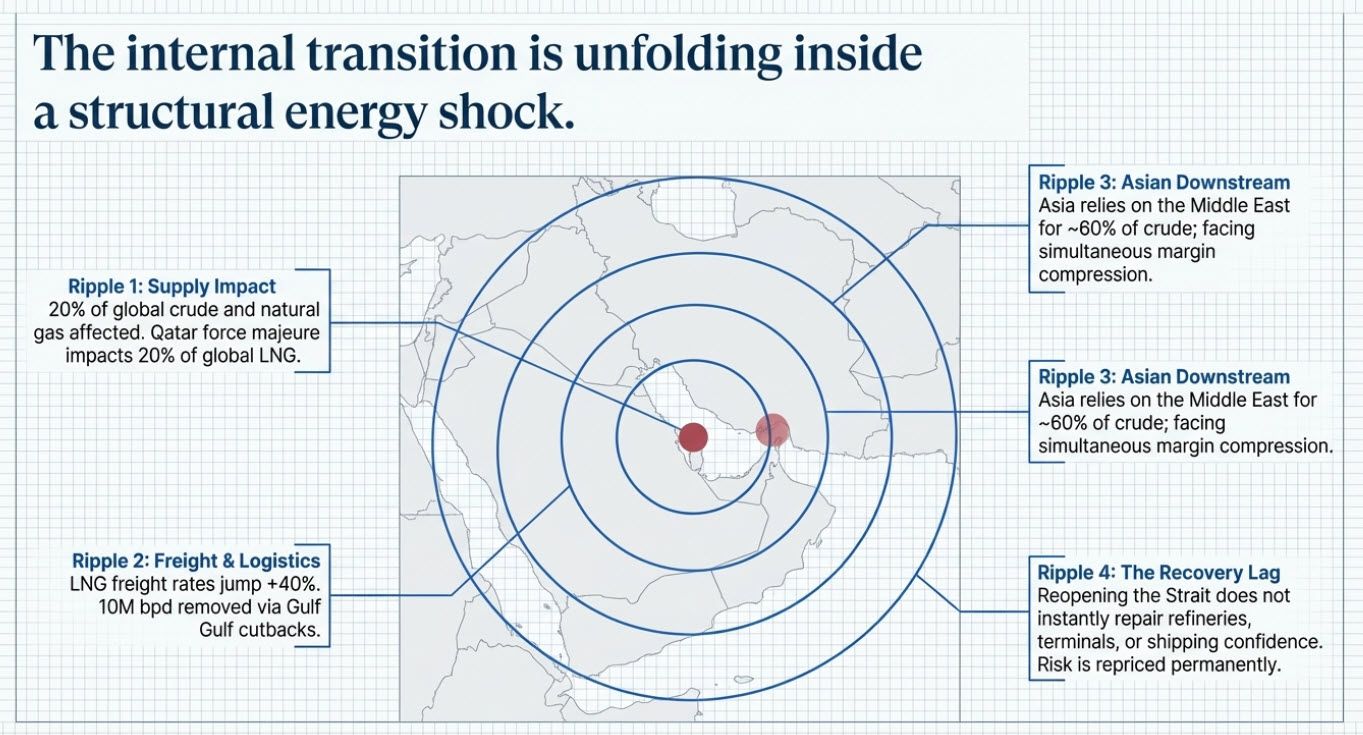

Before any serious assessment of the Iranian internal transition, the external environment has to be understood correctly. Iran is not moving through succession drama in a stable regional setting. This scenario is unfolding amid a historic energy and security shock, and that matters because external pressure shapes internal bargaining.

The Energy Shock Backdrop

The business environment in this scenario is among the most severe energy supply disruptions in modern history. Roughly 20% of global crude and natural gas supply has been affected by the war-linked closure of the Strait of Hormuz, one of the most strategically important chokepoints in the global economy. Qatar’s declaration of force majeure on gas exports after the drone strikes on the Ras Laffan facility matters on its own terms because Qatar supplies about 20% of global LNG. Gulf-wide disruption has also forced Saudi Arabia, Kuwait, Iraq, and the UAE to cut production as storage fills faster than ships arrive. LNG freight rates have jumped more than 40%. Around 10 million barrels per day have been removed from global oil production through Gulf cutbacks alone.

The leadership struggle is unfolding inside a wider shock system that is already repricing energy, freight, and recovery assumptions across the region.

This point matters for executive decision-making. Even a rapid ceasefire does not restore normalcy. Reopening the Strait does not immediately repair damaged refineries, terminals, export facilities, storage networks, or shipping confidence. The repair cycle for damaged energy infrastructure runs in weeks and months, not in headlines and news cycles. That means the pricing regime for energy, freight, insurance, and industrial input costs remains under stress regardless of the political resolution in Tehran. The market is not waiting for ideological clarity. It is repricing risk now.

The IRGC-Junta Negotiation Environment

If the IRGC gains the upper hand and moves toward negotiations with Washington, several structural shifts matter immediately.

First, the negotiation logic favors the IRGC over reformists. The current U.S. demand structure, centered on nuclear rollback, limits on enrichment, reduction of the missile threat, and curtailment of regional proxies, aligns more naturally with a bargaining process conducted by coercive power centers than by weak civilian or reformist actors. A military-led transition offers Washington a counterpart that both controls the machinery of force and has something concrete to trade. The generals would be in a position to offer nuclear concessions, visible de-escalation, and partial restraint in regional conduct. In return, they would seek sanctions relief, economic space, and tacit recognition of their domestic primacy. That is the military-junta deal structure in plain terms. The generals deliver transactional concessions. Washington delivers the economic oxygen needed for regime stabilization. The theocratic shell becomes negotiable or expendable.

The mistake many firms will make is to confuse negotiation with liberalization.

Second, the IRGC’s relationship to sanctions is badly misunderstood in most business analysis. Sanctions have not simply constrained the IRGC. They have also enriched it. They reduced foreign competition, pushed commerce into opaque channels, created black-market premiums, and handed extralegal trade systems to the one institution best positioned to dominate them. The sanctions environment helped justify the resistance economy doctrine, which, in turn, gave the IRGC a national security rationale for absorbing industries and expanding commercial control. This produces a counterintuitive but central point. Partial sanctions relief does not automatically weaken the IRGC. In fact, under a junta framework, it may strengthen the Guard by replacing crude sanctions evasion with more polished, semi-legitimate intermediaries under the same control network. A Western executive who sees sanctions relief and assumes market liberalization will misread the operating reality.

Third, the Egypt model matters because it shows how a military consolidation reshapes market access. After 2013, the Egyptian military did not create an open competitive economy. It marginalized old business elites, denied independent oligarchs meaningful influence over policy, and expanded as a predatory commercial actor in its own right. That is the more useful template for an IRGC-run Iran. The question would not be whether foreign firms are allowed in. The question would be which firms get in, through which gatekeepers, on what terms, through which intermediaries, under what monitoring, with what rent extraction layered into each stage. Market access would not disappear. It would become militarized.

Fourth, any effort by an IRGC junta to negotiate with Washington would require visible distance from Hezbollah, the Houthis, and Iraqi militia networks. But distance does not equal dissolution. This is another point where many analyses stop too early. Proxy networks do not simply vanish because the center changes posture. They fragment, drift, privatize, or turn into semi-autonomous coercive franchises. That produces a different threat map. Instead of a single state-directed proxy architecture, businesses may face multiple armed actors with looser coordination, greater profit-seeking, lower discipline, and greater unpredictability across the Levant and the Gulf.

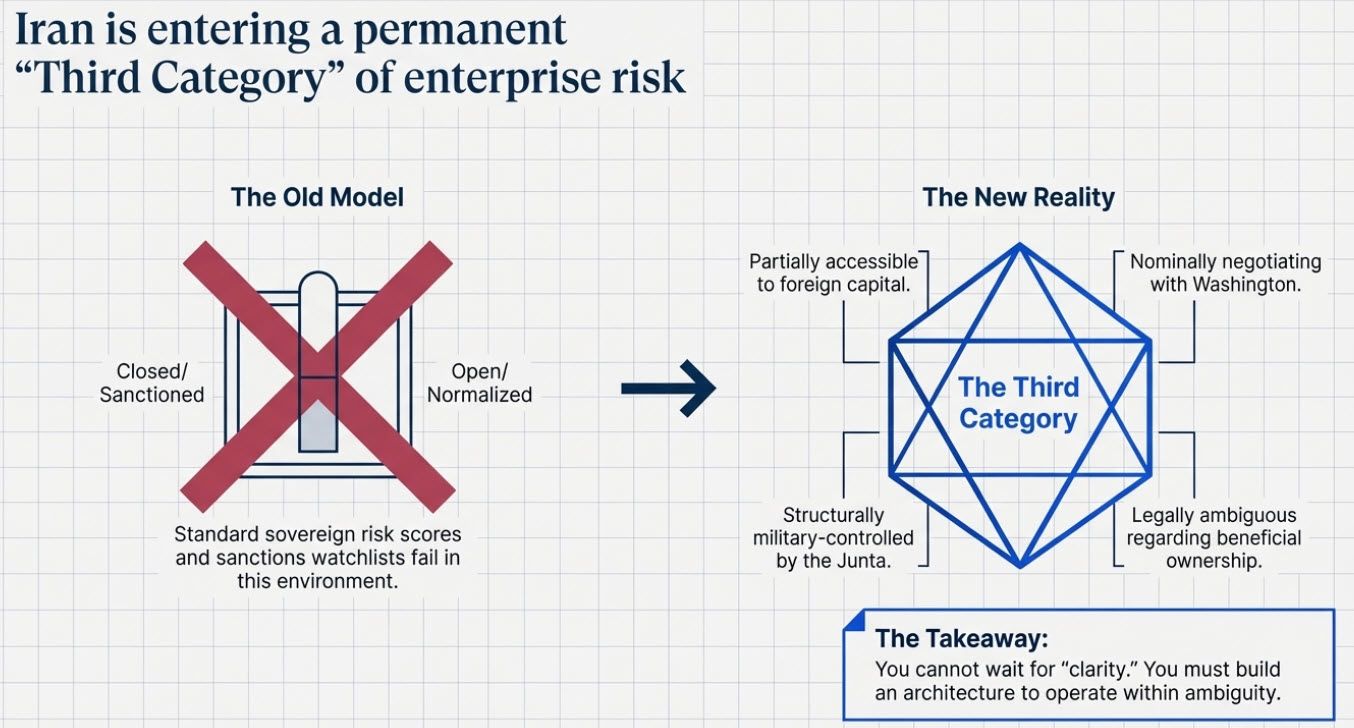

For most firms, the biggest analytical mistake will be treating Iran as either closed or normalized when the more plausible reality sits in between.

What Businesses Need to Plan For

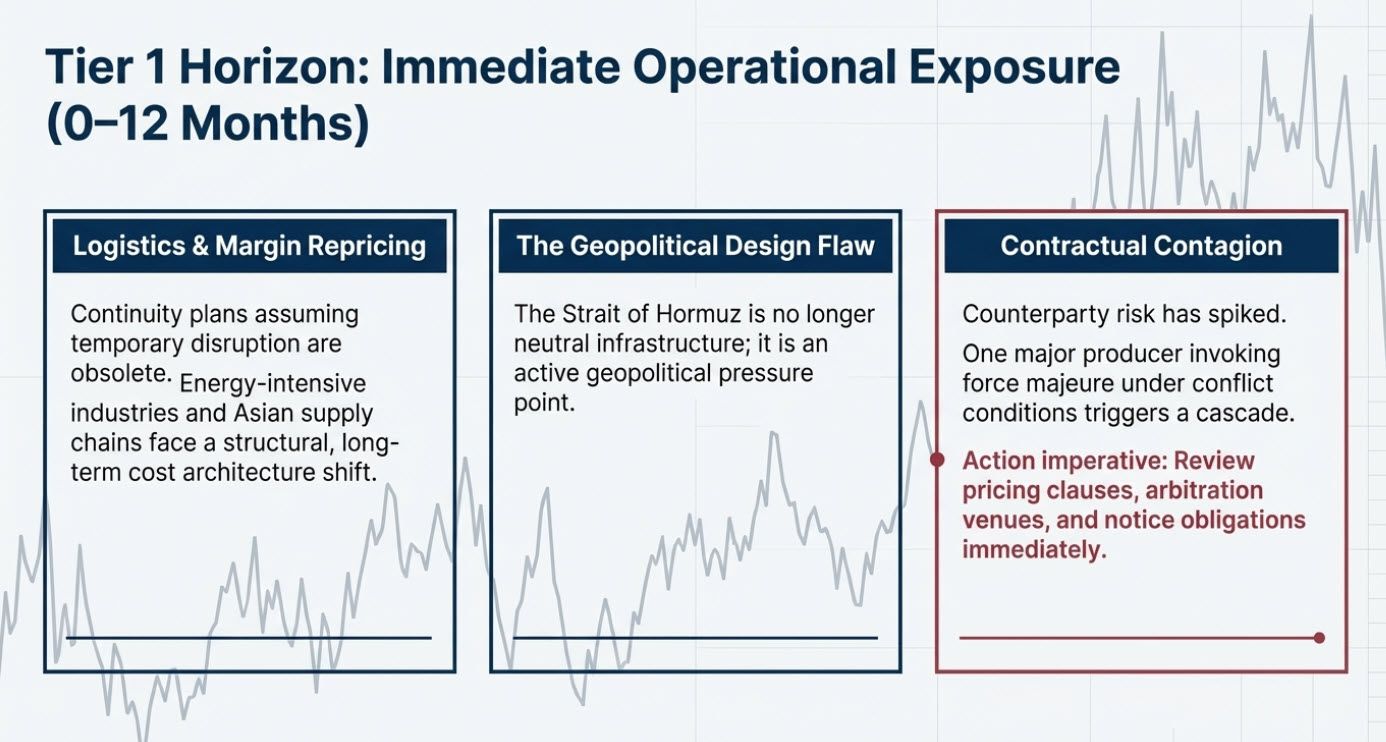

Tier 1 Immediate Operational Exposure, 0 to 12 Months

Energy and logistics costs are not facing a short-lived spike. They are moving through structural repricing. Many continuity plans still assume temporary disruption inside a broadly stable operating range. That assumption no longer fits. Energy-intensive industries, manufacturers, global transport networks, and import-dependent operating models now face a different cost architecture. This is not merely about oil benchmarks. It is about freight, marine insurance, contract repricing, warehousing behavior, inventory strategy, and supplier margin compression all moving together.

At the near-term horizon, the issue is not abstract geopolitical concern. It is immediate operating stress.

The Strait of Hormuz has also exposed a design flaw in many supply chains. Too many operating models treated the Strait as neutral infrastructure rather than as a geopolitical pressure point. Asia’s dependence on the Middle East for about 60% of crude oil means industrial firms across Asia are now absorbing compressed margins, unstable energy assumptions, and operational uncertainty simultaneously. U.S. firms tied to Asian supply chains face a double hit. They face higher input costs for energy and freight, and weaker downstream demand from Asian partners operating under the same strain.

Counterparty risk in Gulf-region contracts has also jumped. Once one major producer invokes force majeure due to conflict, others may follow. Any company with energy supply agreements, infrastructure service contracts, project commitments, shipping obligations, or capital-intensive exposure in the Gulf needs to review pricing clauses, force majeure language, arbitration venues, notice obligations, and operational fallback assumptions. This is not a paperwork issue. It is a cash flow issue.

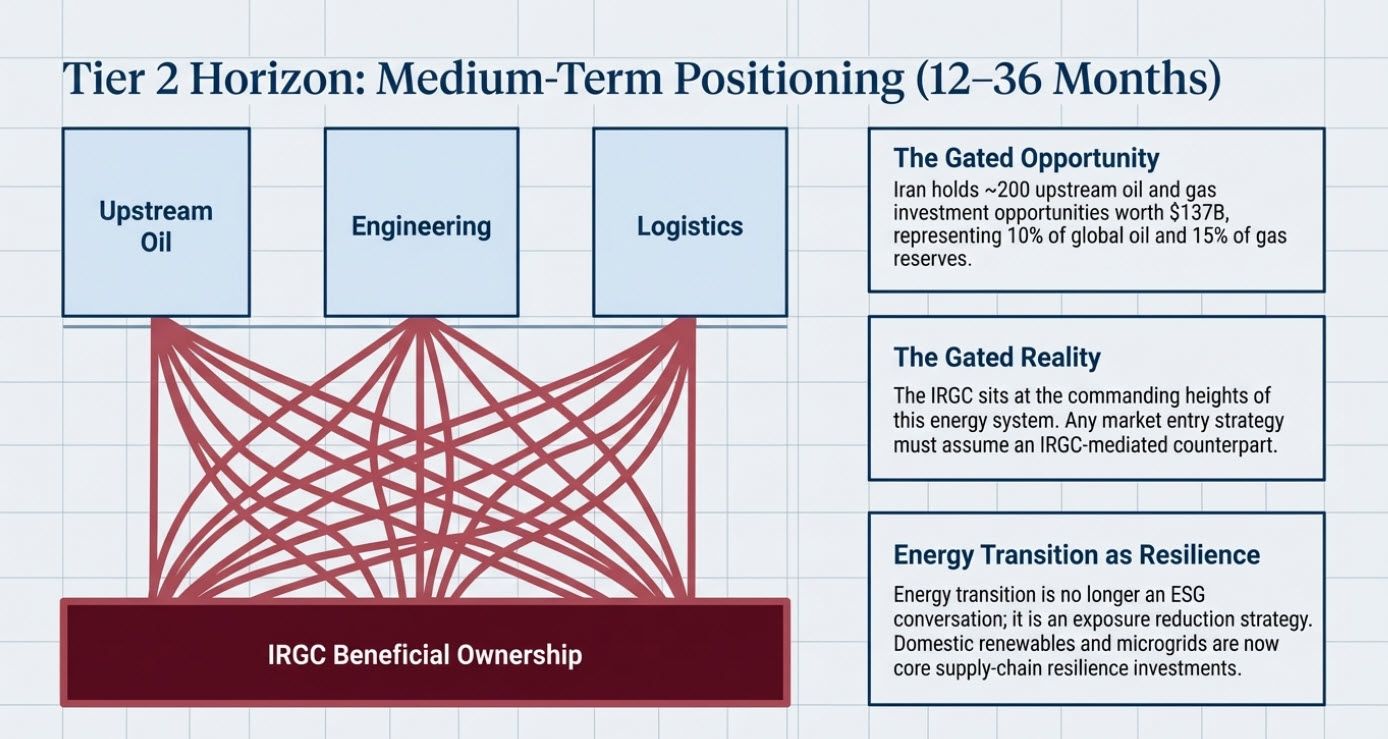

Tier 2 Medium-Term Positioning, 12 to 36 Months

If the scenario advances toward an IRGC-mediated settlement, sanctions relief will not create an open Iranian market. It will create an IRGC-mediated market. Every serious market-entry strategy has to begin from that premise. Any foreign firm seeking access would likely do so through a junta-approved counterparty, intermediary, or commercial structure. The risk is not only direct sanctions exposure under the current law. The deeper risk is opacity in beneficial ownership in a transitional environment where formal structures change faster than real control.

The opportunity set may widen on paper, but the ownership architecture underneath it remains captured.

That point is especially important in energy and infrastructure. Iran has identified roughly 200 upstream oil and gas investment opportunities worth about $137B. The country holds around 10% of the world’s proven oil reserves and 15% of global gas reserves. The reconstruction demand after war damage would be immense. But none of that changes the structural condition of market access. The IRGC sits inside the commanding heights of the energy system. Any serious investment into hydrocarbons, logistics, engineering, terminals, or infrastructure would almost certainly involve IRGC-linked networks as contractual, operational, or beneficial actors. Western executives who treat future opportunity as separate from IRGC entrenchment are treating the visible market and the power structure as unrelated when, in reality, they are the same thing.

This also exposes a flaw in many enterprise geopolitical risk models. Too many firms still assess Iran through a binary lens, sanctioned or not sanctioned. That framework no longer fits the most plausible transition path. The more realistic state is a third category, partially accessible, nominally negotiating, structurally military-controlled, and legally ambiguous. Most enterprise risk systems lack a clear classification for that environment. Sovereign risk scores and sanctions watchlists are not enough. They miss out on front-company exposure, coercive market access, beneficial-ownership opacity, and the possibility that legal permissibility and operating prudence diverge sharply.

The energy transition question also changes in this environment. The war has turned the Strait of Hormuz from an abstract geopolitical talking point into a demonstrated supply chain vulnerability. For industrial firms with ten-year capital planning cycles, domestic renewable generation, storage, grid resilience, microgrids, and energy-efficiency investments now present a stronger strategic case. This is no longer only a values conversation or a climate conversation. It is a resilience conversation. Firms that still think of the energy transition purely through an ESG lens are behind the curve. The better frame is exposure reduction.

Tier 3 Strategic Positioning, 36 Months and Beyond

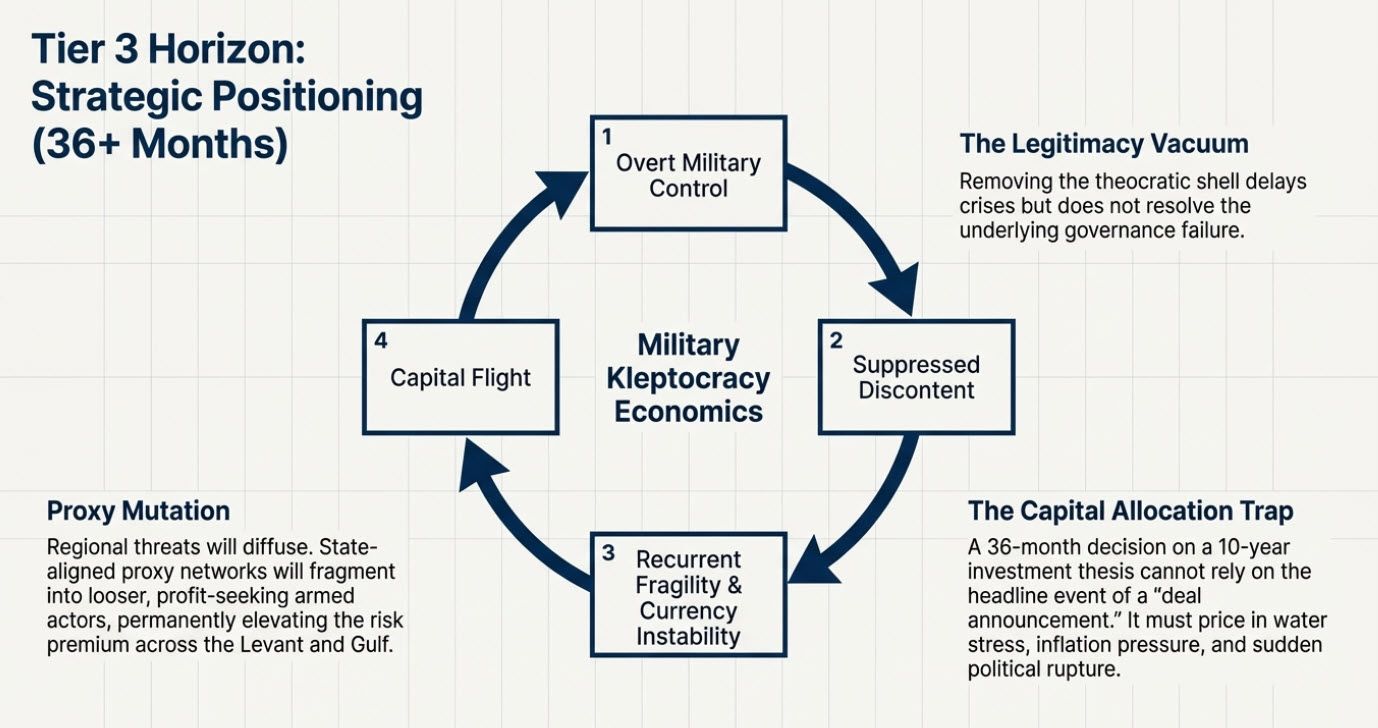

A post-junta Iran would still face a deep legitimacy vacuum. Removing or hollowing out the theocratic shell does not solve Iran’s underlying governance crisis. It strips away one old justification and replaces it with overt military control. That may improve short-term coherence from the standpoint of coercive rule, but it does not produce a stable political settlement. A system built on military enforcement without broad legitimacy has limited capacity for internal correction. It manages discontent through suppression rather than reform. It delays crises rather than resolves them.

Long-cycle investors need to think less about the headline event of a deal and more about the self-reinforcing mechanics of the system that would follow.

That matters for long-cycle investors. Any firm treating Iran as a future infrastructure, energy, finance, logistics, or industrial play needs to ask a harder question than whether Iran opens. The harder question is whether any opening is durable. A military kleptocracy can offer access. It can sign contracts. It can invite foreign capital. But it also produces recurrent fragility, inflation pressure, currency instability, corruption, public despair, water stress, energy shortages, and the constant risk of political rupture. If you are making a thirty-six-month decision on a ten-year investment thesis, those conditions matter more than the headline event of a deal announcement.

The proxy issue also mutates over the long term. Once formal command weakens or fragments, regional threat patterns become more diffuse. Lebanon, Iraq, Yemen, and Syria then carry not only the risk of state-aligned groups, but also looser armed actors pursuing profit, local power, or factional agendas. Those threats are harder to price, negotiate with, and insure against. That shifts the operating environment for any firm with a footprint in the Middle East.

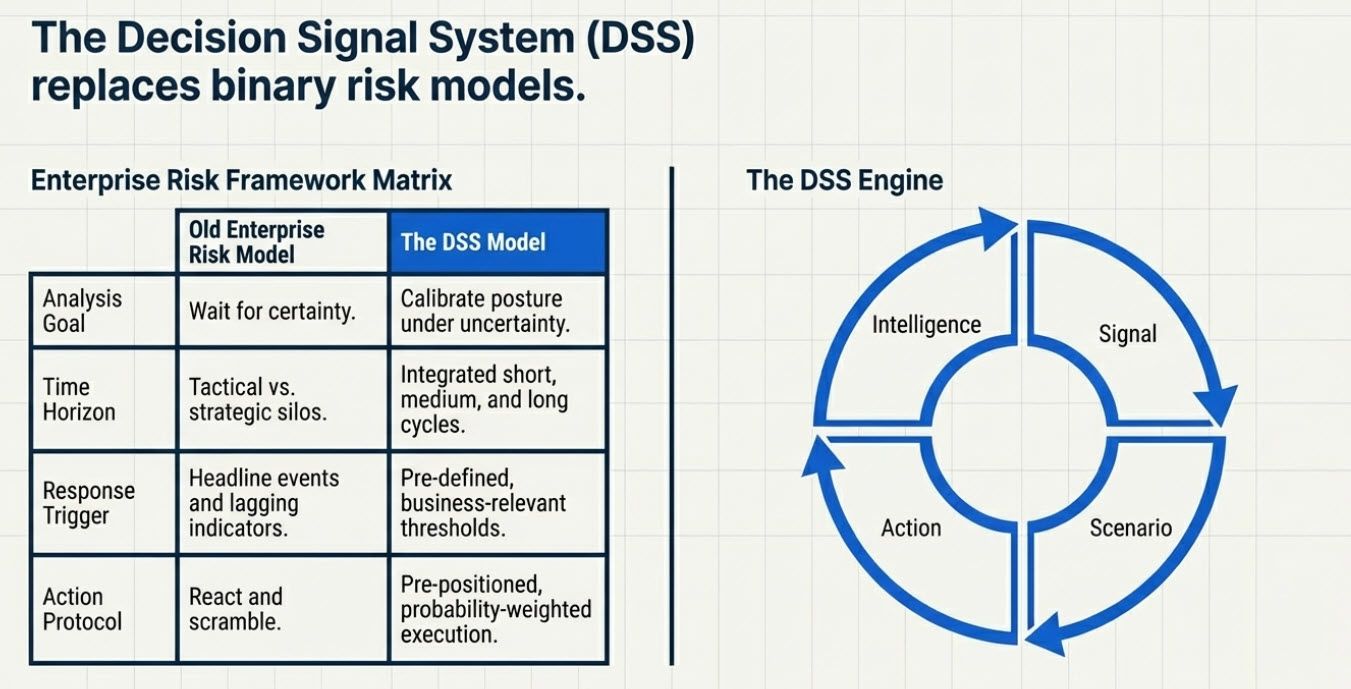

How the Decision Signal System Improves Decision Posture

This is exactly where most enterprise risk models fail. They wait for certainty in an environment that punishes delay.

This is also where a clearer explanation of the Decision Signal System matters, because most descriptions of DSS understate what the framework actually does. DSS is not a dashboard. It is not an alert feed. It is not a loose collection of indicators. It is a structured decision architecture built for uncertain operating environments where the signals are noisy, the actors are competing, and the costs of waiting for certainty are too high.

At its core, DSS does four things.

- First, DSS separates noise from the meaningful signal. In a crisis like Iran’s transition, leaders are flooded with information. Headlines, diplomatic leaks, shipping updates, oil moves, sanctions chatter, militia activity, clerical positioning, and regional military movements all arrive at once. Most organizations process that flow in a fragmented way. One team watches legal risk. Another watches markets. Another watches operations. Another watches regional security. DSS integrates those signal streams into a single decision structure so that leadership does not mistake isolated events for a coherent pattern. The core discipline is not collecting more information. It is filtering signal from noise in a way that changes decision posture.

- Second, DSS translates external developments into business-relevant trigger points. This is one of the biggest gaps in conventional geopolitical analysis. Many briefings accurately describe events but stop short of being actionable. DSS closes that gap. It defines which indicators matter, why they matter, what they imply for the business, what threshold changes decision posture, and what action is tied to that threshold. In other words, DSS does not stop at saying something important happened. It asks what changed, what that means for exposure, and what response should now activate.

- Third, DSS operates across time horizons simultaneously. Most leadership teams split tactical crisis response from long-range strategy. That sounds neat on paper, but in real-world disruption, the tactical and strategic interact constantly. A shipping disruption today changes margin assumptions next quarter. A sanctions shift next month changes market-entry logic next year. A leadership succession event now changes capital allocation assumptions over three years. DSS is built to link those layers. It gives leaders a single framework that integrates short-term, medium-term, and long-cycle implications rather than forcing them into separate conversations.

- Fourth, DSS calibrates posture under uncertainty rather than pretending uncertainty can be removed. This is one of the most important distinctions. Traditional planning systems often wait for clarity. DSS assumes clarity will arrive late, and sometimes not at all. The value, then, is not perfect prediction. The value is preparedness. DSS helps leadership decide how much exposure to accept, what to monitor most closely, where to pre-position options, and what actions to take as probabilities shift. That is what a strong decision posture looks like. Not certainty, but disciplined readiness.

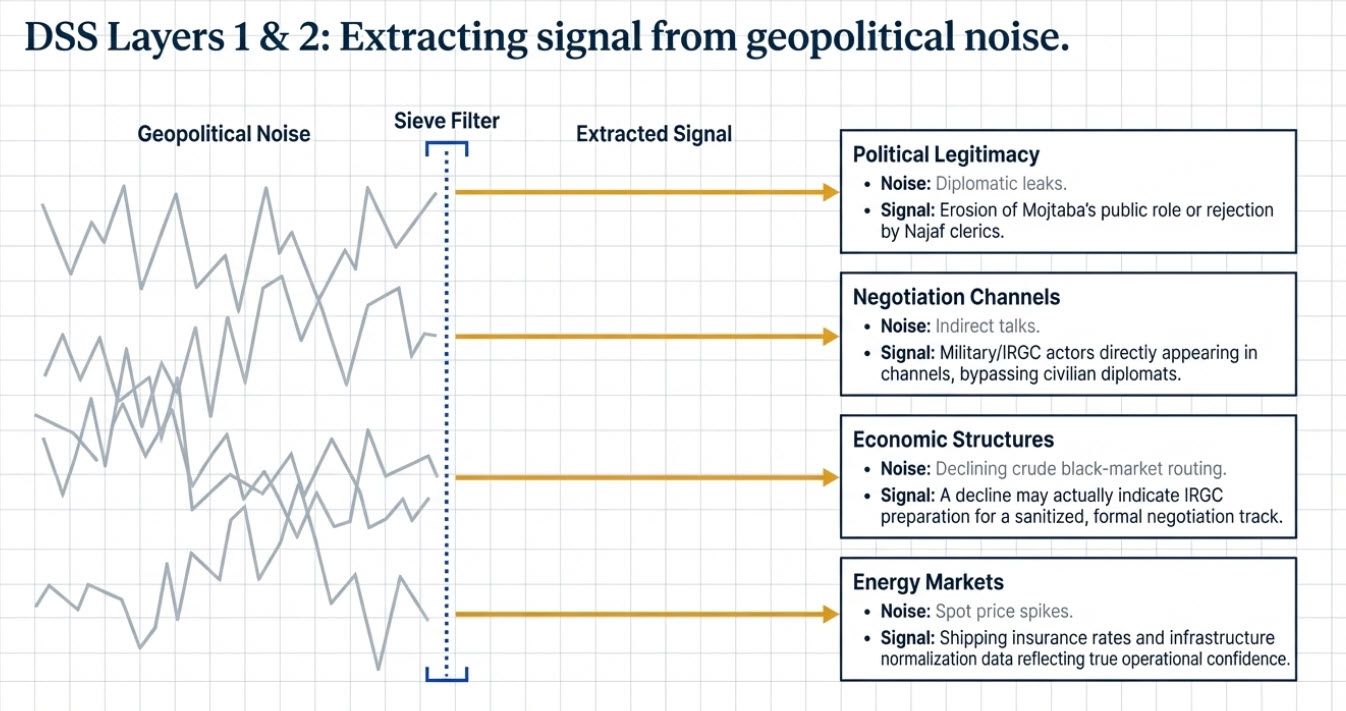

Signal Layer, Monitoring the Transition Triggers

The first layer of DSS in this scenario is signal detection. What observable developments would indicate that the IRGC-junta scenario is advancing, stalling, or splitting into a different path?

Political legitimacy signals come first. Leaders should watch for erosion of Mojtaba’s public role, visible signs of clerical dissent, reduced ceremonial centrality, or the emergence of a leadership-council construct that suggests the IRGC is managing succession from behind a nominal religious shell. The Najaf-Qom divide also matters as a leading indicator. If major clerical authorities outside Iran signal rejection, indifference, or nonrecognition of Mojtaba’s standing, the legitimacy scaffolding weakens faster.

Negotiation signals form the second cluster. Direct or indirect communication to Washington is not enough on its own. The composition of the negotiating channel matters more. If military or IRGC-linked actors begin appearing directly, rather than through traditional diplomatic proxies, that suggests the real center of power is moving into the open. If civilian diplomatic actors retain prominence, the clerical state may still be trying to preserve formal control. DSS distinguishes between the signal event and the meaning of the signal by looking at who is acting, not only at what was announced.

Economic structural signals are the third cluster. Track IRGC-linked commercial activity, especially oil sales through Chinese and Indian intermediaries, shipping patterns, payment structures, and the evolution of front-company behavior. An important DSS principle applies here. A visible decline in crude black-market routing does not automatically mean the IRGC is weakening. In this scenario, it might mean the opposite. It might signal preparation for a more sanitized negotiation track. DSS matters because it helps leaders avoid naïve interpretations of surface-level changes.

Energy market signals form the fourth cluster. Shipping insurance rates, tanker traffic, LNG freight movements, and restoration timelines for damaged Gulf energy infrastructure all function as indicators of whether escalation is being contained, stabilized, or allowed to deepen. Spot prices matter, but they are only one part of the picture. The more valuable signals often lie in insurance, logistics, and infrastructure normalization data because they reflect the market’s judgment of operational confidence.

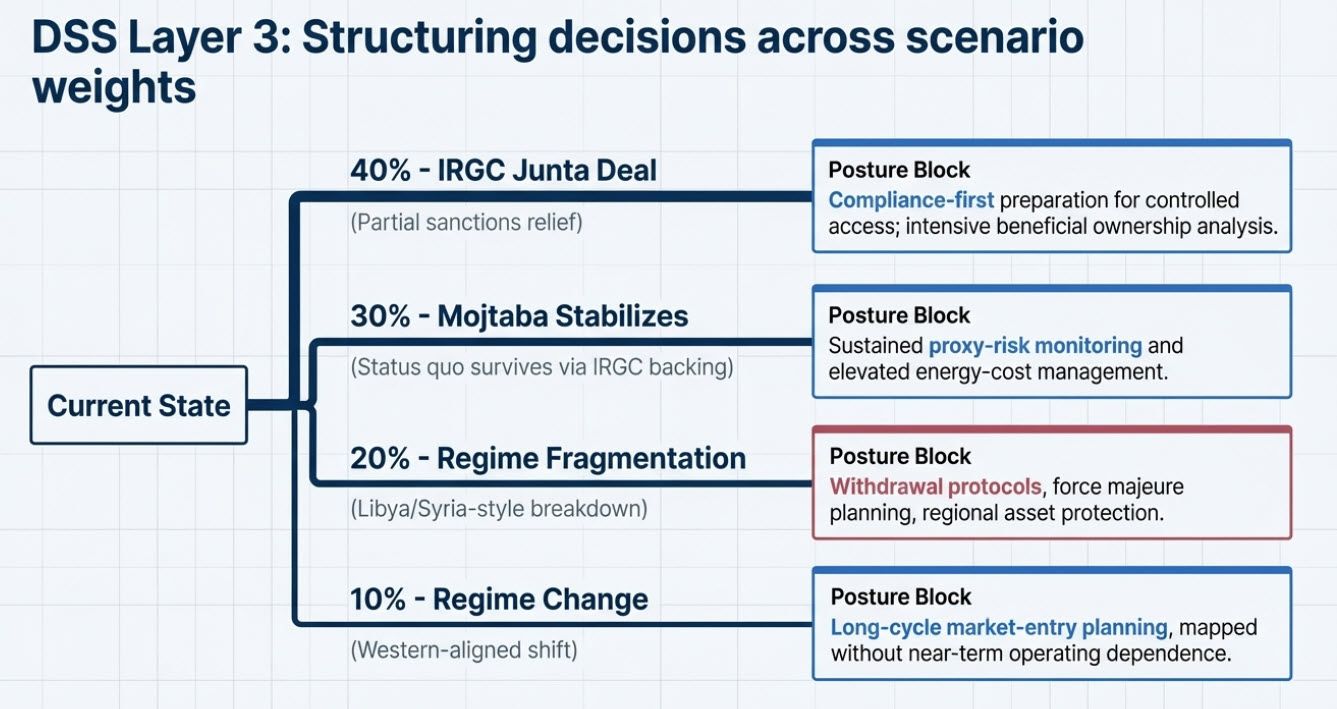

Decision Framework, Scenario-Weighted Posture

A central strength of DSS is that it does not force leadership into one-point forecasting. Instead, it structures decisions across a weighted scenario distribution. That matters because executive teams often fall into narrative lock-in. They pick the most emotionally convincing story and build plans around it. DSS resists that. It keeps multiple futures live and ties posture to probability-weighted exposure.

A strong posture does not depend on calling one future correctly. It depends on preparing for the most plausible distribution of futures.

In this case, the relevant scenario tree has four branches.

- An IRGC junta negotiates a deal, and partial sanctions relief emerges. This is the highest-probability branch at roughly 40%. The right posture under this branch is compliance-first preparation for controlled market access, paired with strong counterparty vetting and beneficial ownership analysis.

- Mojtaba stabilizes with continued IRGC backing, and something close to the current model survives. This sits around 30%. Our posture focuses on continued exposure to sanctions, managing elevated energy costs, and sustained proxy-risk monitoring.

- Regime fragmentation follows, producing a Libya-style or Syria-style breakdown. This is lower, but still material, around 20%. The posture here shifts toward withdrawal protocols, force majeure planning, and protection of regional operations.

- A full Western-aligned regime change occurs. This remains the lowest-probability branch at around 10%. The posture here is long-cycle market-entry planning and relationship mapping, but not near-term dependence on operations.

The point is not the exact percentages. The point is disciplined uncertainty management. DSS keeps leadership from overcommitting to the week's headline scenario.

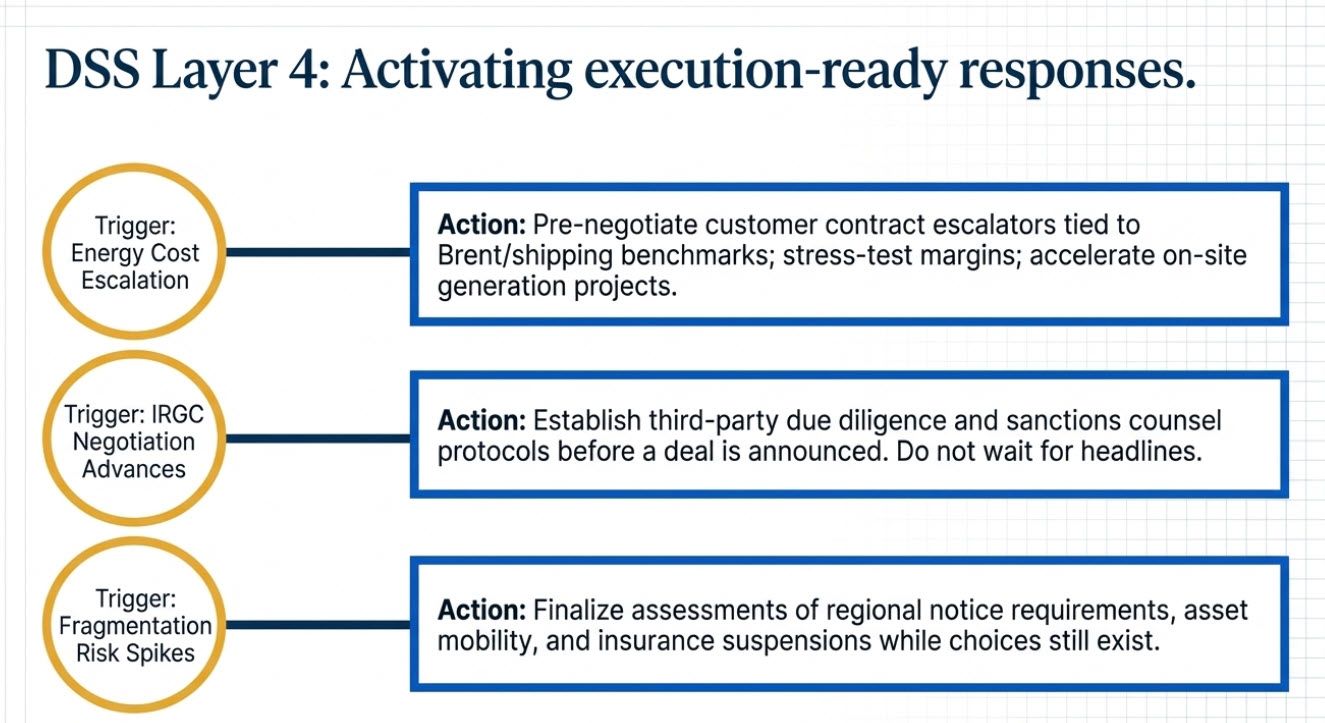

Action Layer, Execution-Ready Responses

DSS also links scenarios to pre-positioned actions. That is where many firms fail. They identify risks, discuss them, and then wait to react. DSS treats action design as part of the analysis itself.

The value of the framework shows up only when monitoring logic is tied to pre-defined execution.

If the energy-cost scenario activates, companies should pre-negotiate customer contract terms with escalators tied to Brent and relevant shipping or insurance benchmarks. They should assess strategic inventory where regulation allows, stress-test margins under extended, elevated inputs, and revisit the speed and economics of on-site generation, storage, and efficiency projects.

If the IRGC-negotiation scenario activates, leadership should already have sanctions counsel, beneficial ownership screening protocols, third-party due diligence methods, and transition-period compliance logic in place before any formal deal is announced. The mistake is waiting for headline sanctions relief and then scrambling.

If fragmentation risk rises, firms need ready assessments of regional contracts, notice requirements, asset mobility, suspension options, personnel protection, and insurance responses. These should not start after the environment breaks. They should be built while choices still exist.

If regime-change risk rises, the preparation should focus on relationship mapping with diaspora networks, development finance institutions, future reconstruction channels, and likely intermediaries in infrastructure and energy. Even then, the posture should remain phased and disciplined rather than euphoric.

Intelligence Layer, What Leadership Should Watch

DSS also imposes discipline on the intelligence function. Not every source deserves equal weight, and not every input should reach the executive level in raw form. The purpose is not information volume. The purpose is signal quality.

Leadership should track credible Iran-focused reporting for internal factional dynamics, specialized energy and shipping data for normalization and disruption signals, sanctions and designation announcements for legal perimeter shifts, serious policy analysis for negotiation-path interpretation, and market-based proxies such as marine insurance and freight indicators for real-time operational judgment. In DSS terms, the question is always the same. Does this information change scenario weight, posture, or required action? If not, it is context, not signal.

The Structural Bottom Line

What this scenario produces is not a new Iran. It produces the existing Iran with less ideological packaging. The IRGC already controls the key levers of security, commerce, border infrastructure, and coercive reach. A military kleptocracy would not create that structure from scratch. It would formalize what has already been taking shape for years. What changes is the interface. Iran would present itself to Washington, markets, and foreign capital through a different front end, one more transactional, less theological, and potentially more legible to outside actors. That surface change is exactly what makes the environment dangerous for firms that mistake presentation for transformation.

A junta-led Iran would still retain anti-American orientation, regional destabilization capacity, nuclear hedging logic, and a kleptocratic economic structure. The risk premium does not disappear. It changes form. Under the old model, firms mostly thought in terms of sanctions compliance. Under the junta model, the dominant risks shift toward counterparty integrity, opacity in beneficial ownership, coercive market access, legal ambiguity, and chronic geopolitical fragility.

The biggest strategic error now would be to treat surface change as systemic change.

That is why DSS matters here more than ordinary geopolitical commentary. Its value is not prediction in the narrow sense. Its value is posture calibration. It gives leadership a way to define which signals matter, what those signals mean for exposure, which scenarios are gaining weight, and what response should already be in motion before the environment becomes undeniable. Iran has spent decades proving that systems under pressure often do not collapse as observers expect. They adapt. The military kleptocracy scenario may be the next adaptation. Firms that read adaptation as reform or access as normalization will misprice risk and pay for that error later.